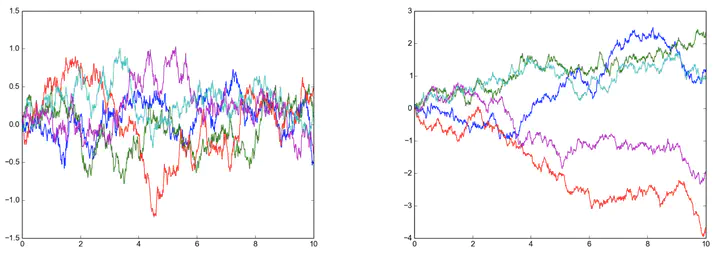

Samples from an Ornstein–Uhlenbeck prior (right) encode drifting back to zero, unlike Brownian motion (left)

Samples from an Ornstein–Uhlenbeck prior (right) encode drifting back to zero, unlike Brownian motion (left)

Abstract

Recently there has been increasing interest in probabilistic solvers for ordinary differential equations (ODEs) that return full probability measures, instead of point estimates, over the solution and can incorporate uncertainty over the ODE at hand, e.g. if the vector field or the initial value is only approximately known or evaluable. The ODE filter proposed in recent work models the solution of the ODE by a Gauss-Markov process which serves as a prior in the sense of Bayesian statistics. While previous work employed a Wiener process prior on the (possibly multiple times) differentiated solution of the ODE and established equivalence of the corresponding solver with classical numerical methods, this paper raises the question whether other priors also yield practically useful solvers. To this end, we discuss a range of possible priors which enable fast filtering and propose a new prior—the Integrated Ornstein Uhlenbeck Process (IOUP)—that complements the existing Integrated Wiener process (IWP) filter by encoding the property that a derivative in time of the solution is bounded in the sense that it tends to drift back to zero. We provide experiments comparing IWP and IOUP filters which support the belief that IWP approximates better divergent ODE’s solutions whereas IOUP is a better prior for trajectories with bounded derivatives.

Hans Kersting

Research Scientist

My research interests lie in machine learning, optimization, and data science.